EPFL spin-offs flourish in a finely tuned ecosystem

A lot of EPFL spin off are located at EPFL Innovation Park© 2017 Alain Herzog

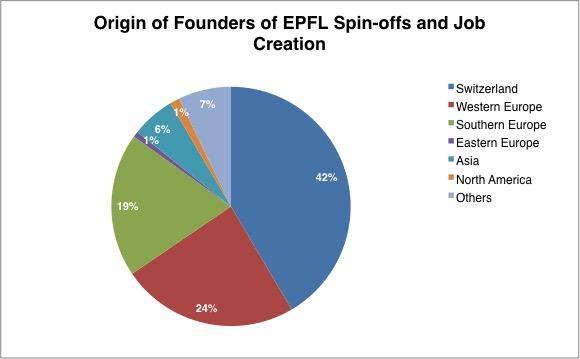

A recent report by EPFL's Vice Presidency for Innovation (VPI) shows just how effective the school’s startup ecosystem is by looking at standard benchmarks such as the number of jobs created, funds raised, and the buyout rate for campus startups. Moreover, successful spin-offs invest in – and even buy out – nascent ones, contributing to the efficiency of this ecosystem hub.

Fast growth is both the goal and common denominator of spin-offs, and the success of a given startup ecosystem is measured through the number of jobs these companies create, the amount of funds they raise and the prices they fetch when taken over. EPFL’s Vice Presidency for Innovation compiled these indicators for EPFL spin-offs in a recent report, which reveals a sharp rise in the number and size of these companies and highlights how some successful startups serve as a model for others.

Startups employ 5–6% of the workforce

According to a recently released study by the Federal Council, the proportion of high-growth enterprises in Switzerland is one of the largest in the world. This is particularly true in the Lake Geneva region, where startups employ 5–6% of the labor force. In the past three years alone, more than 60 spin-offs have been formed in health care, IT and hardware (e.g., robotics, sensors and energy), in near equal numbers across the three fields.

A survey conducted in February among EPFL spin-offs shows that the number of jobs created by these companies has expanded non-stop over the past ten years. Companies founded in 2008 and 2009 currently employ 400 and 350 people, respectively, while companies created in 2016 employ around 50 so far. This pattern stems from the startups’ life cycle: “We know that, up to a certain size, companies that are farther along in the process create more jobs,” says Hervé Lebret, the report’s co-author and the head of EPFL’s startup unit. That means this figure should rise even further in the next few years, since the number of new companies keeps on growing.

Creating a successful spin-off is no walk in the park. Even if the idea is solid and the entrepreneur is highly driven, a number of obstacles invariably get in the way when taking a new technology to the market. Remarkably, the survival rate among EPFL – and ETHZ for that matter – spin-offs is 90% after five years, according to the report, far above the usual rate of around 50%. This may seem like a hallmark of success, but Lebret does not find it particularly meaningful: “In the United States, for example, venture capitalists are often less patient with the startups they back, and startups – which are comfortable with risk-taking – prefer to fail quickly rather than trying to hang on. Europeans, on the other hand, focus more on perseverance.” The slowly but surely approach gives startups the opportunity to benefit from advice, to network and to test their ideas and the market. Along these lines, Lausanne and Zurich have put in place effective structures to help startups get through the difficult growth stage, when they are not yet ready to market their wares – and these cities have been mentioned by the founders of Skype as key players on Europe’s innovation scene.

Buyouts on the rise

The ability to raise money marks a coming of age for startups and shows that their technology has real commercial potential. In the United States, startups rake in 20 to 30 billion francs per year. In Europe, this figure rarely rises above 7 billion. The cultural difference notwithstanding, EPFL spin-offs do quite nicely: they have raised more than 100 million francs per year since 2009, and 70% of that has been in the health-care industry. Previously, this figure never rose above 50 million. This turnaround may have been triggered by the success of Biocartis, a spin-off that raised a record 330 million francs before going public in 2009. That particular accomplishment also prompted startups with no link to EPFL to set up shop on the school’s campus and work in partnership with the labs and other companies there.

Mergers and acquisitions – often involving large companies keen on quickly acquiring a technology rather than coming up with it themselves through costly R&D – are the exit strategy of choice for these young companies. Nine EPFL startups have gone down that road since 2008. These include Lemoptix (which was bought out by Intel), Jillion (Dailymotion) and PlayfulVision (Second Spectrum). The value of these deals is rarely disclosed, but the numbers are surely in the millions. “With a buyout rate of 8%, we are closing the gap with the big US universities, but we're still a long way from the 25% rate seen at MIT and Stanford,” adds Lebret.

A sure sign of success: one spin-off buys another

EPFL’s success has evolved in another direction as well: the campus’ startups are now forming their own financial support ecosystem. And one spin-off, MindMaze, even took that one step further in early June when it bought out Gait Up, which develops motion analysis sensors. Back in 2016, MindMaze raised 100 million francs and then earned unicorn status when its valuation topped one billion before it even went public. News of the buyout was welcomed by EPFL’s technology transfer office, which considers this to be another tangible sign that the startup ecosystem the school so patiently cultivated for the past 30 years is flourishing.